The yield on 2-yr Treasury Notes yesterday dropped to its lowest level ever. As this chart suggests, that means the market has never been so pessimistic about the economy's ability to grow. Short-term Treasury yields typically track the growth of nominal GDP, mainly because they present a risk-free alternative to having exposure to nominal GDP through investments in equities and/or corporate debt. That yields are under 1% for the first time ever suggests the market is expecting that an extended period of recessionary conditions and very low inflation are right around the corner. In other words, 2-yr. Treasury yields provide strong evidence that the economy is already priced to the double-dip recession that so many pundits seem to be calling for.

Let me explain. If nominal GDP is rising 5% a year, for example, then your baseline expectation for the growth rate of corporate cash flows should be something similar. After all, no business can have a cash flow growth rate which exceeds nominal GDP forever, because at some point that business would consume the entire economy. So it stands to reason that on average and over time, corporate cash flows, and profits, will tend to grow by a rate that is close to that of nominal GDP. You can capture that growth rate in your portfolio by holding equity exposure (in the hopes that growth will be positive and you will earn more than 2-yr Treasury yields), or by buying the 2-yr. Treasury if you're not sure and don't want to take any risk.

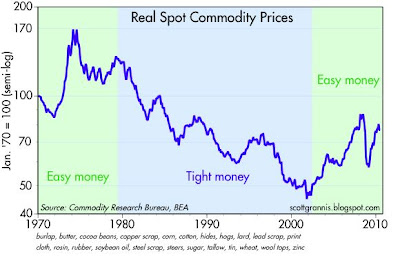

This chart is also instructive because it shows that yields tended to equal or exceed nominal GDP from the early 1980s through the early 2000s. That same period happened to be one in which inflation was generally falling and relatively low. It was also the same period during which the Fed almost always proclaimed that it was pursing a restrictive monetary policy (which involves pushing interest rates up relative to inflation so as to increase the demand for money). But beginning in 2002, the Fed began pursuing an overtly accommodative monetary policy, and this translated into yields generally being less than the growth of nominal GDP.

When 2-yr Treasury yields exceed the growth rate of nominal GDP, investors are naturally drawn to financial assets (e.g., cash, Treasuries), because they tend to outperform nominal GDP on a risk-adjusted basis. But when yields are less than nominal GDP, investors tend to prefer investments which are tied to the physical economy (e.g., commodities and real estate), since they tend to outperform the returns on financial assets. Corporate bonds and equities do especially well when money is tight and real yields are high, because in a tight money environment yields tend to fall and inflation stays low; falling yields make the return on equities look attractive, and so investors tend to bid up PE ratios; PE ratios tend to be highest when growth and inflation are lowest. Low inflation also tends to discourage investments in real assets (like real estate and commodities), and by doing so, low inflation discourages speculation and instead encourages investments in productive activities; low inflation thus tends to lead to stronger growth.

The fact that we've had easy money for most of the past 7-8 years helps explain why equities have performed poorly—with PE ratios declining of late—and corporate bond spreads are still historically wide. It also explains the strong performance of commodity prices, and—until a few years ago—the strong performance of real estate.

I have said this many times before and I'll say it again: the two most significant headwinds facing the economy today (and for the past year) are faux-stimulative fiscal policy and excessively "easy" monetary policy. (This of course flies directly in the face of the common perception that the economy has only managed to recover thanks to stimulative fiscal and monetary policy.) The huge expansion of government regulations and spending under the Obama administration, the fact that most of the spending took the form of transfer payments, and most of the tax cuts were temporary rebates, coupled with the Fed's $1 trillion injection of bank reserves via the purchase of MBS, have done almost nothing to increase hard work and risk taking, while greatly increasing investors' uncertainty regarding the future. How high will taxes have to rise to restore some semblance of sanity to the budget? How can spending be throttled back without creating even more pain and suffering? How high or low might inflation be in the future?

The great economist Allan Meltzer has an excellent op-ed in today's WSJ titled "Why Obamanomics Has Failed." Read it, since it adds a lot more substance to my sparse remarks on fiscal policy here.

It's important to note that these headwinds have been with us for some time, and they help explain why the economy has experienced a sub-par recovery to date. Business investment is improving on the margin, but as I have pointed out before, investment is severely lagging the rise in corporate profits, and a lack of confidence in the future surely helps explain why.

Does this mean we are doomed? No. It's always dangerous to extrapolate recent trends into the future, and that is especially the case today. There is a sea-change underway in the public's willingness to tolerate larger and more intrusive government, and this will very likely result in some huge changes to policy in the wake of the November elections.

Meanwhile, as the chart above suggests, the economy is moving in a positive direction, and the fears of a double-dip recession which have brought the equity market down may well prove to be unfounded. Holding cash or short-term Treasuries because one expects the economy to collapse may prove to be a very expensive hedge, not least because yields on risk-free investments are very close to zero, while yields on alternative investments (equities, corporate bonds, etc.) are historically high.

{kind=link}